Nearsightness

Credit cards are seen as an “adult thing” that are not necessary at millennials’ current life stage especially because credit products fail to communicate the value proposition and long- term benefits of credit card use.

We compared a variety of financial products, explored emerging fintech, investigated Mastercard's B2B2C business model, and mapped users' current credit journey.

We conducted interviews and generated design ideas through brainstorming and co-design workshops. We validated concepts by testing prototypes with target users.

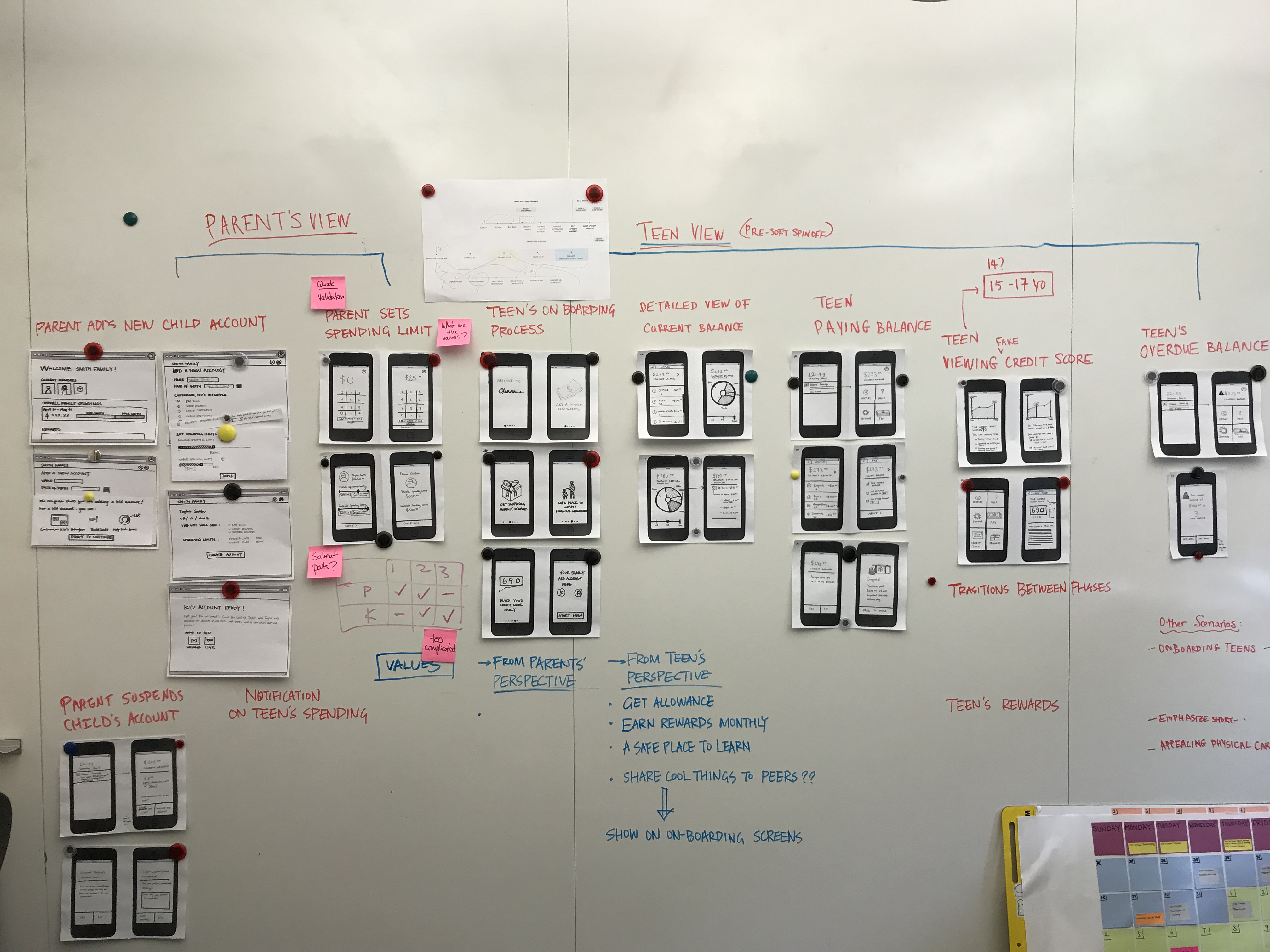

We iterated on our design to build low, medium and high fidelity prototypes. We got feedbacks from multiple Mastercard's internal stakeholders.

We explored the world of credit from user, technology, and business perspectives. We interviewed more than 30 people, conducted a co-design workshop, and synthesized our findings using affinity diagrams, a concept selection matrix, and user personas.

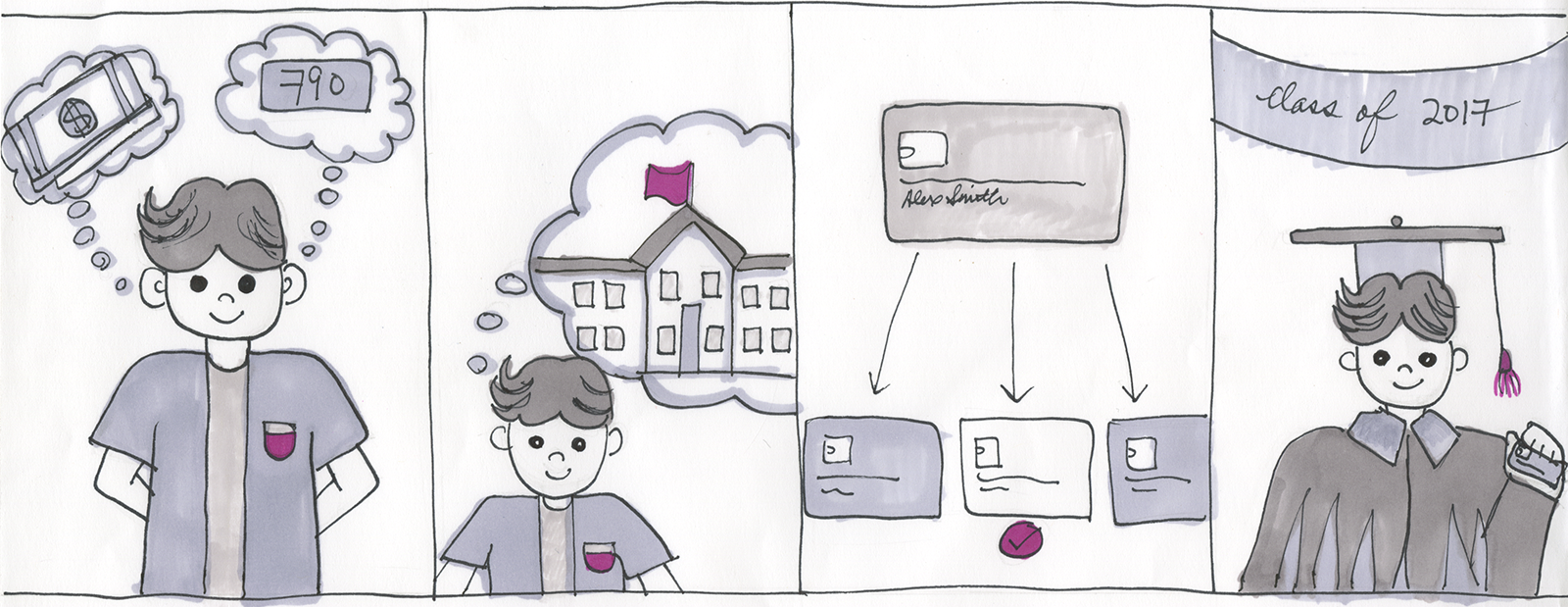

Millennials represent a large market opportunity currently underserved by credit card companies. Millennials have the lowest rate of credit card ownership among any demographic, with only 1 in 3 holding a credit card in their pocket. For these users, the question is not which card is top-of-wallet, but how to get a card there to begin with.

We created physical prototypes in response to each identified pain point. We validated these concepts using these artifacts and storyboards through a speed-dating session.

Below are some of the early prototypes we made.

In an ideal situation, a "universal profile" revolutionizes the entire credit card ecosystem and makes Mastercard become users' lifelong companion. However, requiring Mastercard to change their current B2B2C business model in the near future is unrealistic.

Even if we want to solve the bigger problem, we still need to keep the problem within a managable scope. Our idea for a family plan boosts teenagers' financial journey with parental guidance, fights against fear of credit, and helps them gain confidence.

We want to educate teenagers to be financially independent. Ohana fills a gap in the competitive landscape of credit training products.

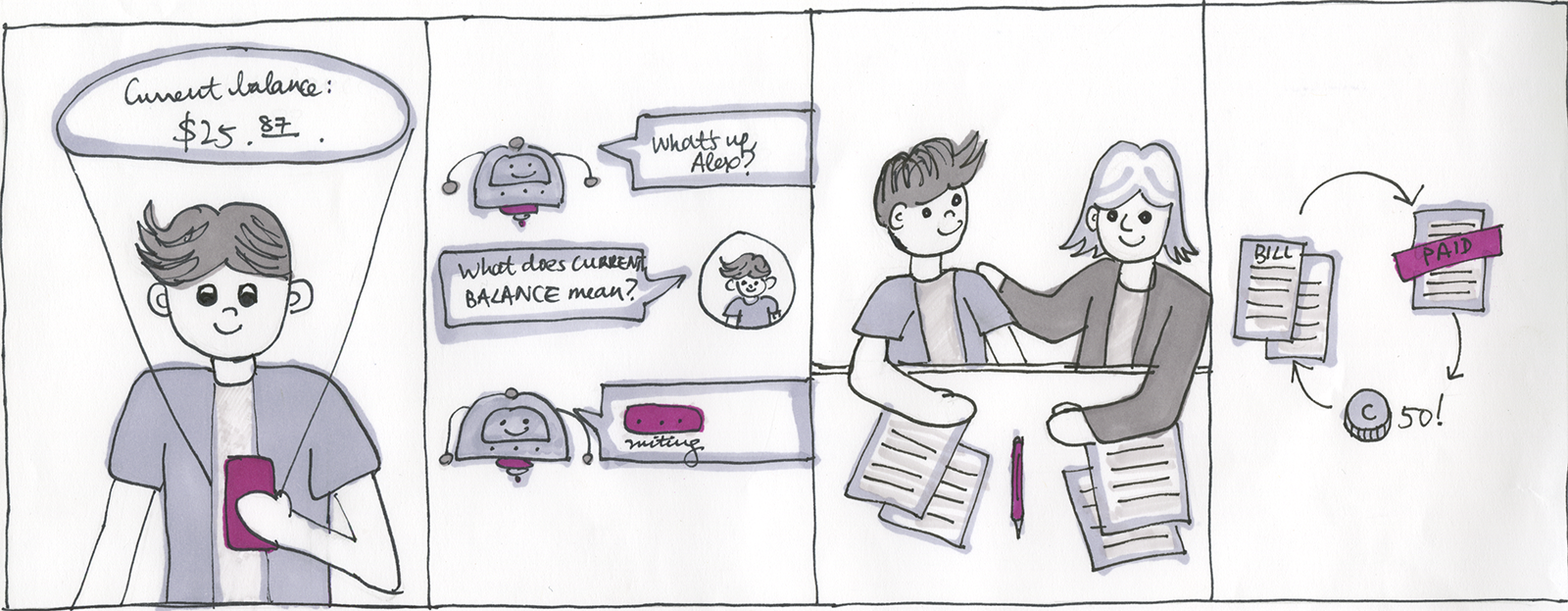

Motivation: Novice users must understand the long-term bene ts of credit in order to use their credit cards responsibly.

Habituation: Novice users must be trained to adopt healthy behaviors like checking their balance regularly and staying within their budget.

Basic Knowledge: Novice users must learn basic terminology like “balance” and “APR”.

We started to learn how young people understand financial empowerment from various aspects. We asked them to link their current financial fears and concerns on a mind map. We learned that confusing payment process, messing up credit scores, and lack of financial conversation with parents are three main problems.

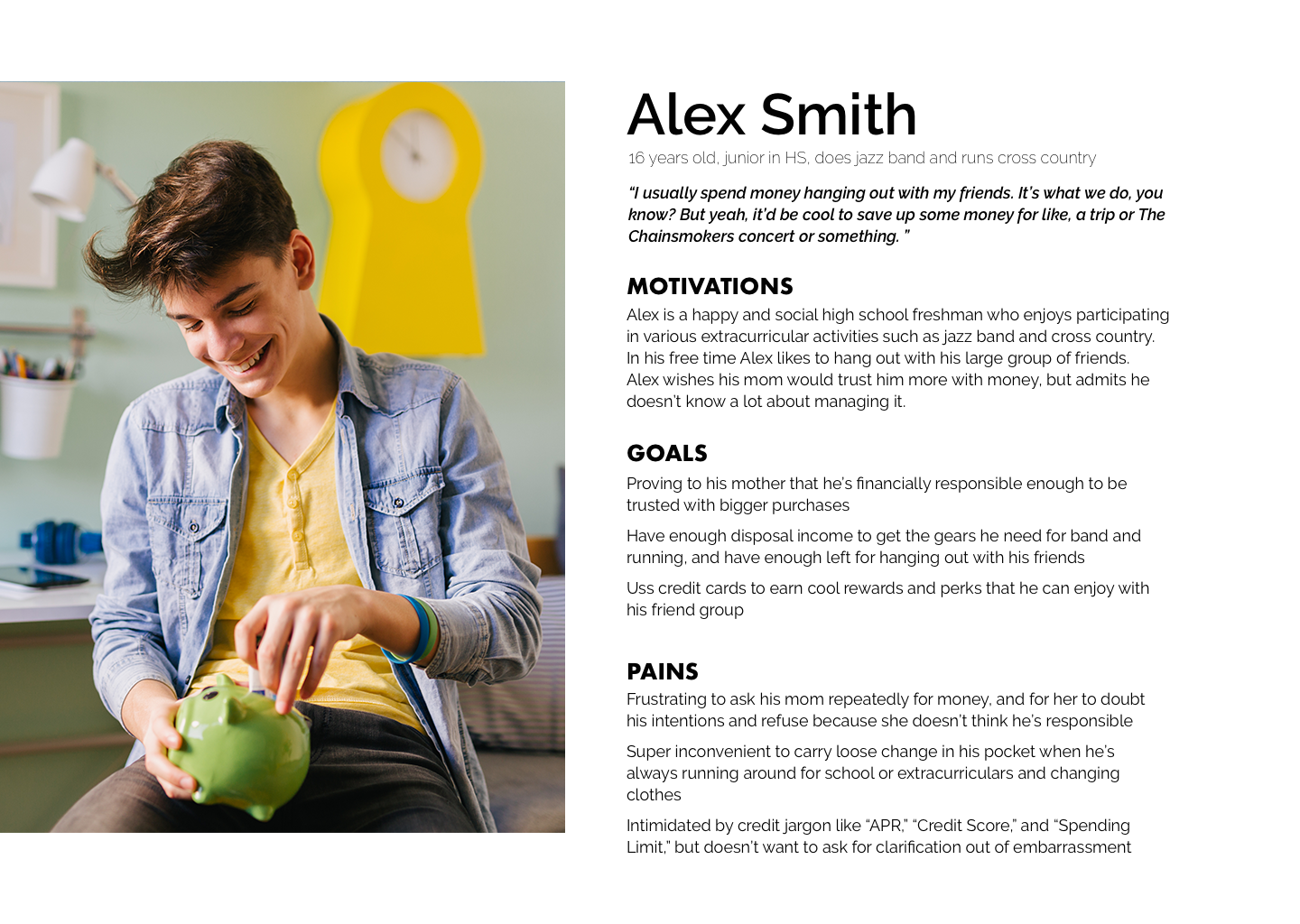

Alex is a happy and social high school sophomore who enjoys participating in various extracurricular activities. In his free time Alex likes to hang out with his large group of friends. Alex wishes his mom would trust him more with money, but admits he doesn’t know a lot about managing it.

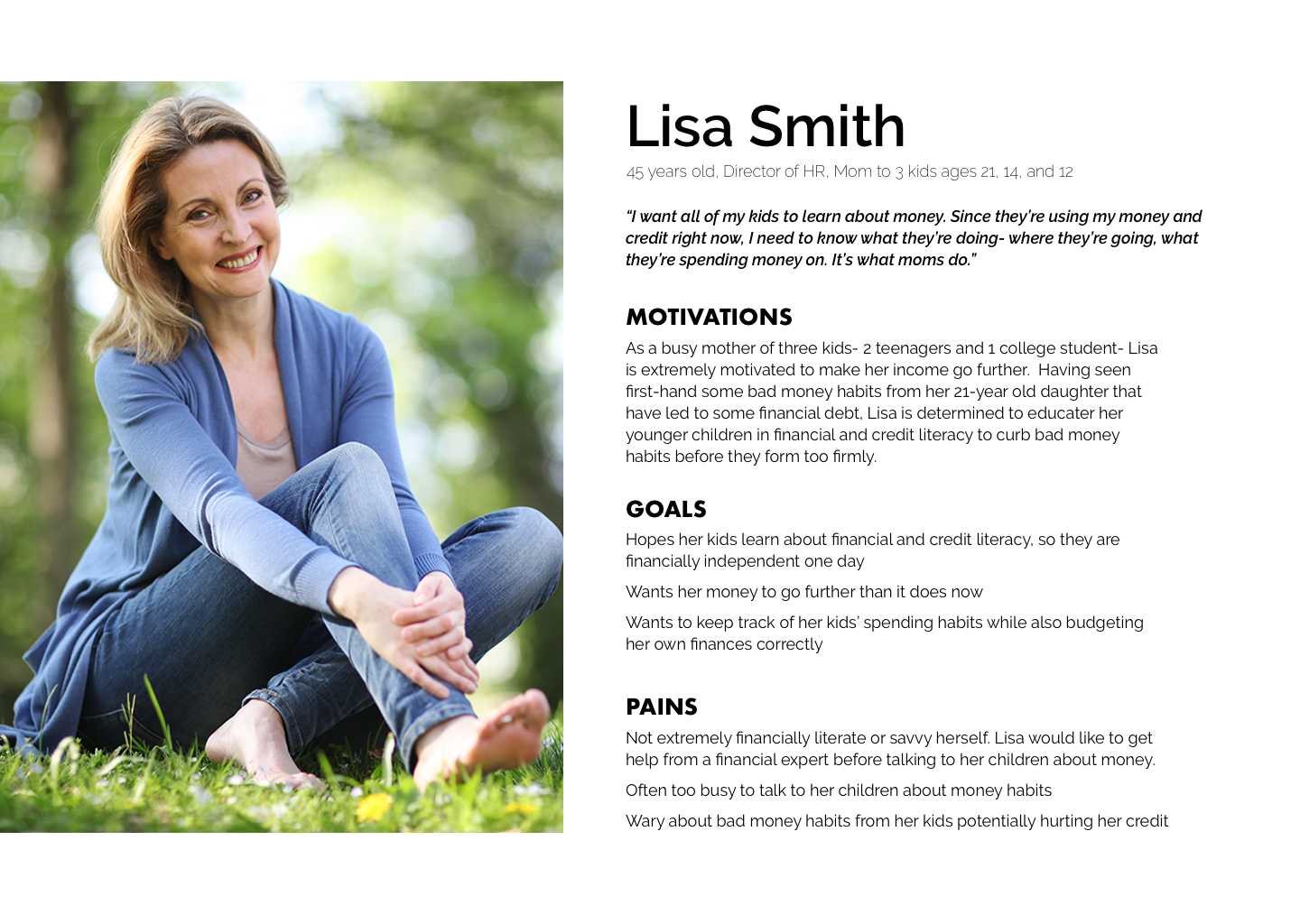

As a mother of three kids, Lisa is extremely motivated to make her income go further. Having seen first-hand some bad money habits from her 21-year old daughter that have led to some debt, Lisa is determined to educate her younger children in financial and credit literacy.

Level 1: Beginner

Parents and teenagers register and teenagers use a pre-paid debit card that functions like a credit card. Teenagers' credit scores will not be affected, and parents will have a high level of control over their children's spending.

Level 2: Intermediate

Designed for teenagers with basic financial knowledge. Teens will have cosigned credit cards and Ohana will protect their credit scores in various ways. Parents will have intermediate level of control over the account.

Level 3: Advanced

Teens get a full-fledged credit card. They will be financially literate enough to successfully manage their accounts. Ohana enables them to get more advanced cards that they wouldn't have access to otherwise.

We validated the concepts using card sorting exercises and storyboards with parents and teenagers. We listed the features that parents and teens would want, and asked them to cluster these features.

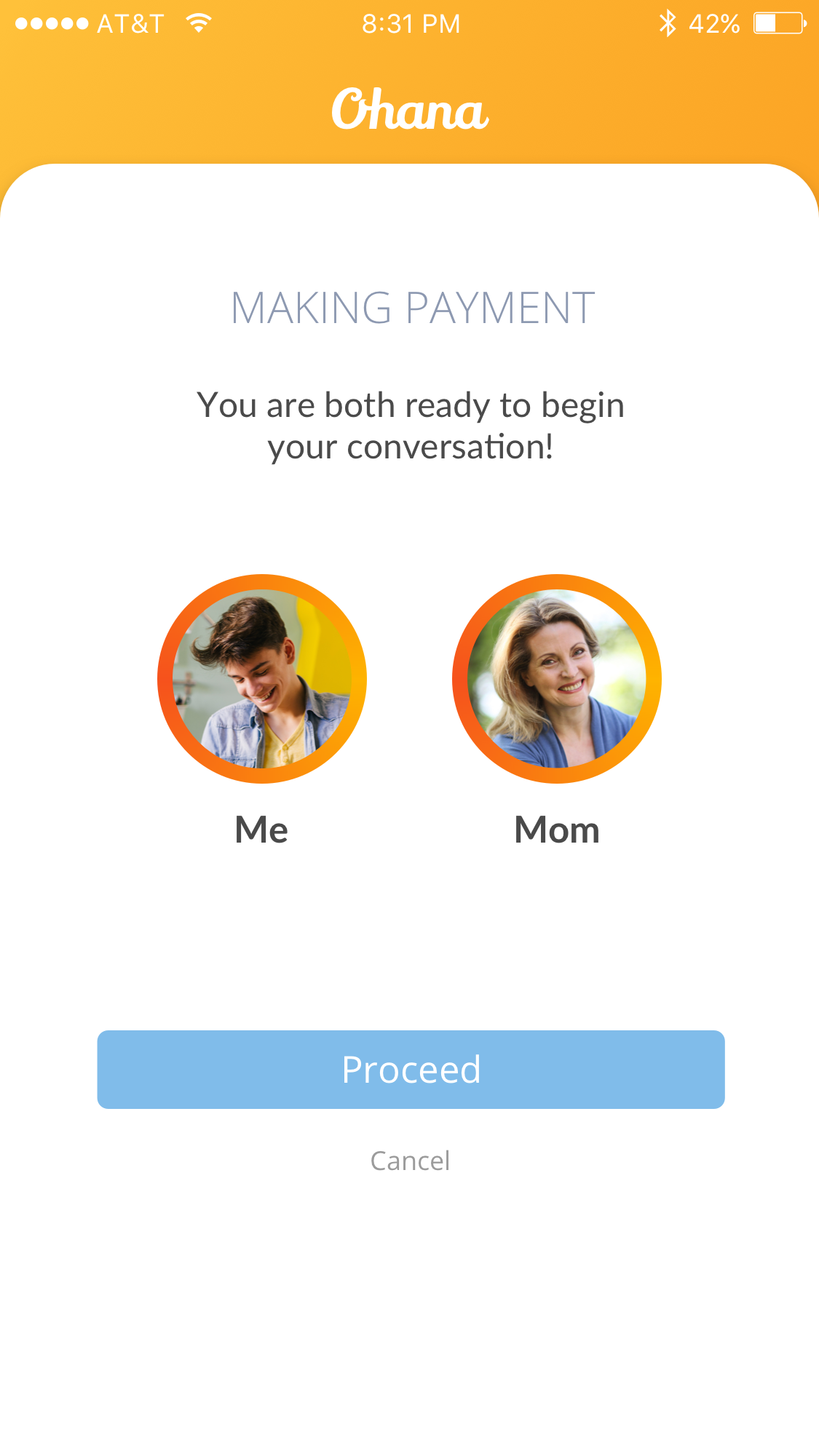

The whole Ohana experience includes the teenager's card and mobile apps for the parent and the teenager. We prototyped all of them iteratively, and tested the usability with teenagers and college students.

We prototyped the entire process from onboarding to graduation. Going well beyond the standard design of banking apps, we invested in novel educational activities, gamification, data visualization, and aesthetic personalization.

We had to strike the right balance between parental control and teen independence.

Giving too much parental control can interfere with teen learning and engagement.

The app explains complex terms and conditions in an easy and interactive way and projects future financial states.

Users will get in the rhythm of paying every month.

Teenagers can view an analysis of their own spending with detailed breakdown by category.

Teenagers get rewards for showing responsible behavior.

Users can earn more rewards by completing various financial activities with their parents.

We presented the designs to Mastercard internal stakeholders from various departments. Their feedback helped us further hone the user experience and marketing strategies of Ohana, as well as our skills on how to successfully pitch a product.